You need cash by Friday, the situation is real, and you don't have the luxury of someone scolding you to "just save more." You needed that buffer last month, not now. So let's skip the lecture and do the useful thing: walk through how to borrow money safely in an emergency, cheapest options first, with the exact questions to ask before you sign and the traps to refuse outright.

Plenty of people are exactly where you are. Federal Reserve data has found that a large share of adults couldn't fully cover a $400 emergency with cash, and a smaller group couldn't cover it by any means; our piece on covering a $400 emergency digs into the numbers. Needing to borrow doesn't make you irresponsible. It makes you human in a tight spot. The goal here is to borrow without getting wrecked.

First, is borrowing even the right move?

Before you borrow a dollar, do a 30-second gut-check: is there a cheaper way through this that isn't a loan at all? Sometimes there is, and it's worth the two minutes to look.

- A payment plan with the biller. Medical offices and utilities often spread a bill out for free.

- Assistance programs. Dial 211 for local help with rent, utilities, and food, or call the LIHEAP energy hotline at (866) 674-6327.

- An employer advance on wages you've already earned, sometimes available with no interest.

If one of those covers it, you've solved the problem without taking on debt at all. If they don't, then borrowing is a legitimate choice, and the rest of this is how to do it safely. (If the bigger issue is too many bills at once, start with our plan for what to do when you can't pay your bills.)

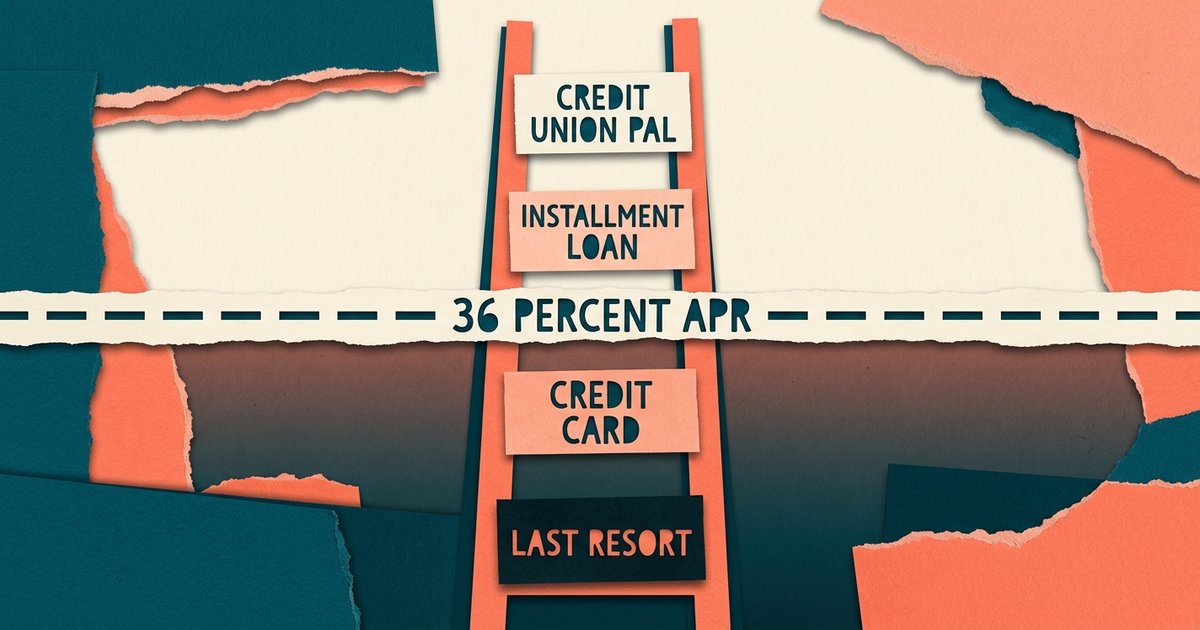

The options ladder, cheapest to most expensive

When you do borrow, start at the top of this ladder and only move down if the rung above isn't available to you. The order matters, the difference between the top and bottom is the difference between a manageable bill and a trap.

- Credit union Payday Alternative Loan (PAL). Federal credit unions can offer PALs designed as a safe alternative: PAL I runs $200 to $1,000, PAL II up to $2,000, both capped at 28% interest with an application fee of no more than $20, over terms of 1 to 12 months (NCUA, MyCreditUnion.gov). This is usually the best deal on the ladder. Availability depends on the credit union and membership, so it may not be open to everyone.

- A personal or installment loan from a bank, credit union, or reputable lender. You repay in fixed installments over time, which is far safer than a single balloon payment.

- A credit card you already have, if the APR is reasonable and you have a real plan to pay it down. Not ideal, but predictable.

- Last resorts. Avoid single-payment payday loans designed to be repaid in one lump from your next paycheck. That structure is what creates the trap, which we'll get to.

The 6 questions to ask before you sign

Whatever you're about to sign, get clear answers to these six questions first. A legitimate lender will answer all of them plainly and in writing. If they dodge, that's your answer.

- What's the total I'll repay in dollars? Principal plus all interest plus all fees, not just the APR. Get the real number.

- What's the full repayment schedule? How many payments, on what dates, and how are they collected?

- Is there a prepayment penalty? You want the right to pay it off early for free.

- What happens if I'm late? The exact late fee and the collection process.

- Does it report to the credit bureaus? If it does, on-time payments can actually help your credit.

- Am I skipping a cheaper option? A credit union PAL, an employer advance, a payment plan, an assistance program.

The 36% rule of thumb

Use 36% APR as your rough line between a reasonable loan and a predatory one. That number isn't arbitrary. Under the Military Lending Act, lenders generally can't charge service members and their dependents a Military APR above 36%, can't impose prepayment penalties, and can't force arbitration (CFPB, Military Lending Act). Congress drew that line because rates above it get dangerous fast.

One honest note: that 36% cap legally protects service members, not all civilians. For everyone else, treat it as a benchmark, not a law that's protecting you. If a loan's APR is well above 36%, slow down and look harder at the ladder above. The credit union PAL, capped at 28%, sits comfortably on the safe side of that line.

Red flags that mean walk away

Some signals mean stop, no matter how badly you need the cash. Refuse a loan that shows any of these:

- An upfront fee before funding. Legitimate lenders take their fees from the loan, not from you in advance. "Pay us first" is a scam pattern, not a normal one.

- "Guaranteed approval" regardless of credit. Real lenders evaluate. A guarantee is bait.

- Pressure to roll over or renew. Anyone nudging you to "just renew" wants you in the cycle, not out of it.

- No written disclosure of the APR and total cost. The Truth in Lending Act requires real lenders to disclose terms. No paper, no deal.

- A single balloon payment from your next paycheck. This structure is built to fail so you'll borrow again.

The FTC keeps plain-language guidance on spotting loan scams and your disclosure rights (FTC, credit, loans, and debt). When in doubt, walk. A real opportunity survives you taking a day to think. Our deeper guide to "guaranteed approval" and other red flags covers the scam playbook in detail.

How the debt trap actually forms

It helps to see the trap clearly, because it doesn't feel like a trap on day one. It feels like relief. Then the single payment comes due, you can't cover it and rent, so you "renew" the loan for another fee, and now you owe the original amount plus that fee, and the clock resets.

The CFPB has documented this as the rule, not the exception: the large majority of payday loans are rolled over or reborrowed within two weeks, and most borrowers who roll over end up owing as much or more than they originally borrowed. That's the cycle in plain terms: a $400 problem becomes a months-long obligation that costs multiples of what you borrowed. Our breakdown of the hidden APR of a payday loan shows the math behind it. An installment loan or a credit union PAL, with fixed payments and no balloon, is how you avoid it.

Borrow it, then build a buffer so you don't have to again

Once the emergency's handled, the move that keeps you off this ladder next time is a small cushion. Even $500 in a starter emergency fund is what turns the next surprise into an errand instead of a loan application. And a flexible 50/30/20 budget built on your real income is where that savings finds room to grow. You don't have to build it all at once, you just have to start it after this.

How matching works here

If a fixed-installment loan is the right tool for your emergency, you can see what loan options may be available through our request form. A few things you deserve to know plainly: American Cash Relief is a lender-matching service, not a lender. We don't make loans, we don't make credit decisions, and we can't guarantee approval or any particular rate or term. Rates and terms come from the lenders themselves and vary by your situation. Seeing your options is a soft step that doesn't affect your credit score; a hard inquiry only happens if you choose to formally apply with a specific lender. Use this page like you'd use any tool, with the checklist above in hand, and walk away from anything that trips a red flag.

Frequently Asked Questions

What's the least dangerous way to borrow money in an emergency?

Start at the top of the options ladder: a credit union Payday Alternative Loan (capped at 28% interest with a fee of no more than $20), then a personal or installment loan with fixed payments, then a credit card you already have. Avoid single-payment payday loans, which are built to be rolled over.

Is a payday loan ever okay or always a trap?

The single-payment payday loan structure is what creates the trap. CFPB research found the large majority are rolled over or reborrowed within two weeks. A credit union PAL or an installment loan with fixed payments is almost always a safer way to cover the same emergency.

A lender wants a fee before giving me the loan. Is that normal?

No, that's a red flag. Legitimate lenders take their fees from the loan itself, not from you upfront. Demands for an advance fee before funding are a common scam pattern; walk away.

How do I know if a loan's interest rate is too high?

Use 36% APR as a rough dividing line. The Military Lending Act caps rates for service members at 36% because rates above it get dangerous. For civilians it's a benchmark, not a legal protection, so treat APRs well above 36% as a reason to look harder at cheaper options.

What questions should I ask before signing an emergency loan?

Ask for the total you'll repay in dollars, the full repayment schedule, whether there's a prepayment penalty, the exact late fees and collection process, whether it reports to credit bureaus, and whether you're skipping a cheaper option. A legitimate lender answers all six in writing.

Need cash before payday?

Pick your amount and get matched with lenders in our network. It's free, secure, and there's no obligation.